WHY GOVERNMENT CREATED RCM?”

Why did the Government create Reverse Charge Mechanism (RCM)?

Forward Charge Mechanism (FCM)The Regular Way

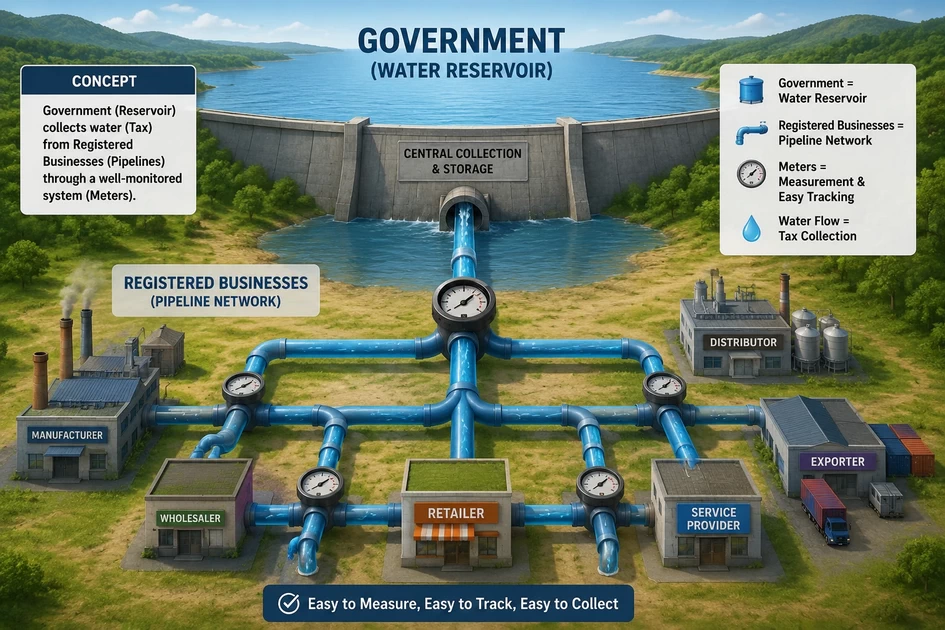

Imagine a massive water reservoir (the Government) collecting water from a major pipeline network (Registered Businesses). The pipeline has built-in meters, so tracking the water flow is easy.

Reverse Charge Mechanism (RCM)?

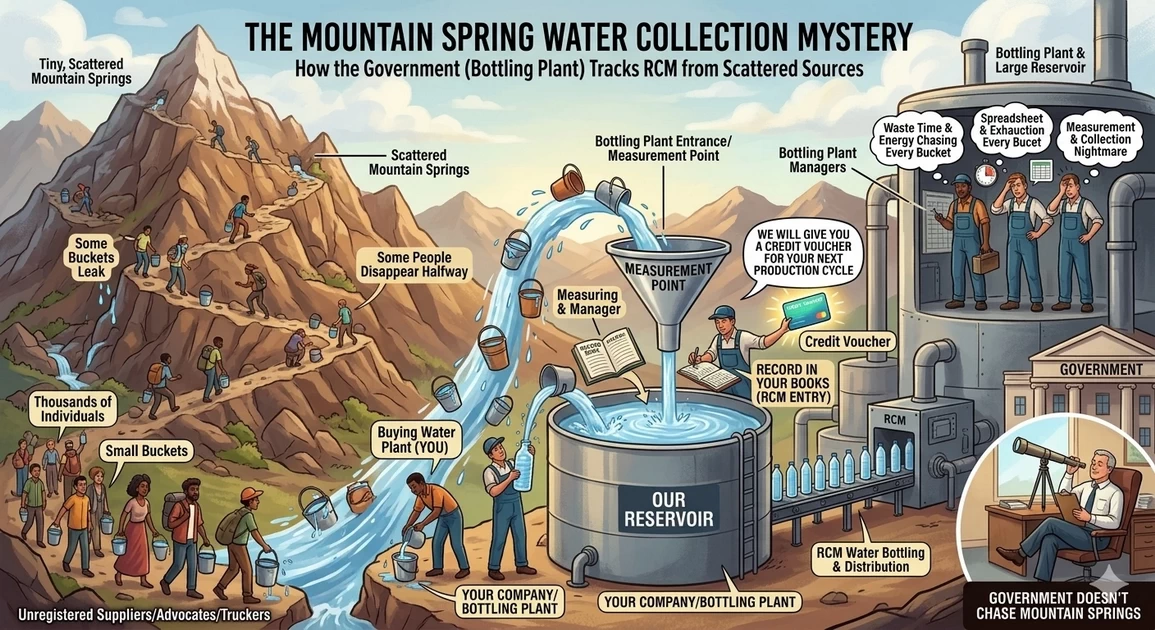

Now imagine thousands of individuals fetching water from tiny, scattered mountain springs using small buckets (Unregistered Suppliers/Advocates/Truckers). Some buckets leak, some people disappear halfway, and the reservoir managers waste massive amounts of time and energy running around trying to measure and collect from every single bucket.

The RCM Solution:

The reservoir managers change the rule. They tell the large water bottling plants (The Registered Buyers): “Whenever you buy water from those scattered mountain springs, you must measure it yourself, pour it directly into our reservoir, and record it in your books. In return, we will give you a credit voucher for your next production cycle.”

By doing this, the government doesn’t have to chase the mountain springs. The bottling plant does the tracking for them.

Why Government Introduced RCM?

Government introduced RCM for:

- Better tax collection

- Control on unregistered transactions

- Tracking special services

- Preventing tax leakage

FCM- NORMAL GST

Buyer → Pays GST → Seller → Pays GST → Government

RCM

Buyer → Pay GST Directly → Government

“In RCM, GST responsibility flips upside down!”

SECTION 9(3) FIRST

THE GOVERNMENT FACES A PROBLEM

Imagine there are:

- Thousands of advocates

- Small Transporters

- Freelancers

- Unregistered suppliers

- Local contractors

- Director remuneration

- Import of services

GOVERNMENT THINKS:

“How can we track lakhs of small people individually?”

This becomes difficult because:

- Some may disappear

- Some may not file GST

- Some may under-report income

- Tracking cost becomes huge

Government says:

“Whenever these services come, buyer should pay GST.”

WHY BUYER?

Because buyer is usually:

- Big company

- Registered business

- Easy to track

- Maintains accounts properly

- Files GST regularly

Government trusts big businesses more than scattered small suppliers.

RCM applied.

BEST MEMORY TRICK

Now say dramatically:

“Section 9(3) was about service type…”

“But Section 9(4) is about UNREGISTERED PEOPLE.”

“RCM is not just accounting entry. It is Government’s smart strategy to collect tax from organized businesses instead of chasing scattered small suppliers.”

Tally Prime Practical Assignment: RCM Mastery

Company Profile Setup

Create a fresh company in Tally Prime:

-

Company Name:

Blooming Logistics & Retail Private Limited -

State:

Tamil Nadu -

Financial Year:

1-Apr-2026 -

GSTIN Configuration: Enable GST (

F11$rightarrow$ Taxation) and input a valid Tamil Nadu corporate format GSTIN (e.g.,33AAAAA1111A1Z1). Ensure “Enable Reverse Charge Calculation” is set to Yes.

📅 The Assignment Transactions (Month: May 2026)

Your students must process the following four sequential transactions. Each transaction tests a specific practical accounting skill.

Transaction 1: Booking a Notified Service under Section 9(3)

-

Date: 5th May 2026

-

Scenario: The company hired QuickMove Goods Transport Agency (GTA) to bring raw materials from Chennai to the Trichy warehouse. QuickMove GTA issued Consignment Note No.

QM-8891for ₹15,000. As per GST law, GTA services under the 5% option are subject to RCM, where the recipient pays the tax. -

Tally Task:

-

Create Vendor Ledger:

QuickMove GTAunder Sundry Creditors (Registration Type: Registered). -

Create Expense Ledger:

Freight Charges (GTA)under Indirect Expenses. Set GST to Applicable, specify details, choose Taxable at 5%, and set Is Reverse Charge Applicable to Yes. -

Record via F9: Purchase Voucher (Accounting Invoice Mode).

-

Transaction 2: Booking an Unregistered Expense under Section 9(4)

-

Date: 12th May 2026

-

Scenario: The office required urgent printing repairs and maintenance. A local freelance technician, Mr. K. Perumal, executed the job and gave a handwritten bill (Bill No.

KP-99) for ₹8,000. He is completely unregistered under GST. -

Tally Task:

-

Create Vendor Ledger:

Mr. K. Perumalunder Sundry Creditors (Registration Type: Unregistered). -

Create Expense Ledger:

Office Repairs & Maintenanceunder Indirect Expenses. Set GST to Applicable, specify details, choose Taxable at 18%, and set Is Reverse Charge Applicable to Yes. -

Record via F9: Purchase Voucher.

-

Transaction 3: Tax Liability Booking (Statutory Adjustment)

-

Date: 31st May 2026

-

Scenario: It is the end of the month. Before filing GSTR-3B, the accountant must formalize the unbooked RCM liability into the company’s General Ledgers.

-

Tally Task:

-

Go to

Display More Reports$rightarrow$Statutory Reports$rightarrow$GST Reports$rightarrow$GSTR-3BorReview RCM Liability. -

Note the total RCM tax liability computed by Tally for both transactions.

-

Press

Alt+J(Stat Adjustment) inside a Journal Voucher. -

Nature of Adjustment: Increase in Tax Liability & Input Tax Credit.

-

Additional Details: Process separate or combined entries to debit/credit CGST and SGST ledgers appropriately.

-

-

Debit: CGST & SGST (Creating our Tax Asset)

-

Credit: CGST & SGST (Creating our Tax Liability)

-

Value: ₹1,095 each.

Transaction 4: RCM Government Settlement (Payment)

-

Date: 31st May 2026

-

Scenario: The company settles its monthly tax liabilities. The calculated RCM liability is paid out using the company’s current account online.

-

Tally Task:

-

Go to F5: Payment Voucher.

-

Use Auto Fill (

Ctrl+F) or selectStat Payment. -

Debit CGST and SGST ledgers to nullify the current liability, and credit State Bank of India (Current A/c).

-

The Final Balance Sheet Reveal: Take them back to the Balance Sheet. The Duties & Taxes will now show a clean $(-)2,190$.

“The minus sign under liabilities means it is a Debit balance. It is no longer a debt; it is a permanent tax credit asset sitting in our pocket for our next regular sales billing!”

FAQ

What is the Reverse Charge Mechanism (RCM) in GST?

The Reverse Charge Mechanism (RCM) is a tax compliance process under GST where the liability to pay tax shifts from the supplier to the recipient of goods or services. In a standard transaction, the seller collects tax from the buyer and deposits it with the government. Under RCM, the seller does not charge tax on the invoice; instead, the buyer calculates the tax amount, pays it directly to the tax authorities, and issues a self-invoice.

Can we claim Input Tax Credit (ITC) on RCM payments?

Yes, a registered business can claim Input Tax Credit (ITC) on the tax paid under the Reverse Charge Mechanism. However, you can only claim this credit if the goods or services were used for business or furtherance of business. Additionally, the credit can only be claimed in the month after the RCM liability has been successfully discharged to the government in cash.

Can RCM liability be paid using an existing Input Tax Credit balance?

No. Under GST law, you cannot use your existing Electronic Credit Ledger (ITC balance) to pay off an RCM liability. The tax due under the Reverse Charge Mechanism must be paid strictly in cash using the Electronic Cash Ledger during your monthly GSTR-3B return filing. Once paid in cash, that exact amount is added to your ITC ledger for future adjustments against outward supplies. “To see a visual step-by-step demonstration of how this cash ledger adjustment reflects in a journal entry, check out our detailed RCM Tally Prime video tutorial below.”

When is RCM applicable for businesses?

RCM is primarily triggered in three scenarios:

When a registered business purchases goods or services from an Unregistered Dealer (URD).

When a business procures specific notified services, such as legal services from an advocate, Goods Transport Agency (GTA) services, or sponsorship services.

During the import of services from a provider located outside India.